Francisco Rodríguez[1]

Josef Korbel School of International Studies

University of Denver

In recent days, the US government authorized Chevron Corporation to resell Venezuelan oil in US markets but barred it from making tax and royalty payments to the Venezuelan state. We argue that the restriction on these payments is symbolic because fiscal liabilities are incurred not by Chevron but by the joint ventures in which Chevron is a minority partner and whose decisions it is unable to control. Furthermore, we show that as long as regaining access to US markets enables Chevron joint ventures to increase production levels, the Maduro government will receive additional hard currency revenue flows which it can use at will. This result holds regardless of whether incremental revenues are used to reduce PDVSA’s debt arrears with Chevron.

On November 26, the Treasury Department’s Office of Foreign Assets Control published a license allowing Chevron to significantly increase the scope of its operations in Venezuela. Up until that time, Chevron – the sole American company directly involved in extracting and selling Venezuelan oil – had been restricted to performing activities necessary for maintaining or winding down essential operation but was barred from producing or selling Venezuelan oil. The new license – labeled Venezuela General License No. 41 in the OFAC nomenclature – now allows transactions related to the production, lifting and sale of Venezuelan oil into the United States, as well as the purchase and importation into Venezuela of the intermediate inputs needed to carry out these activities.

However, General License 41 also explicitly bars the payment of any taxes or royalties to the Government of Venezuela or the payment of dividends to any entity owned by the Venezuelan national oil company, Petróleos de Venezuela, SA (PDVSA). The US Treasury Department published a press statement claiming that the authorization “prevents PdVSA from receiving profits from the oil sales by Chevron.” A Biden administration official told the New York Times that instead of going to pay taxes and royalties, profits earned would go to the repayment of government debt to Chevron.

We argue that statements claiming that the Maduro administration will not receive revenues from the oil sales allowed by General License 41 are either factually incorrect or highly misleading. Furthermore, the US government’s mischaracterization of consequences for Venezuelan fiscal accounts of the granting of this license is a serious impediment to the design of the mechanisms of accountability necessary to ensure that the funds obtained by Venezuela as a consequence of sanctions relief are used to attend Venezuela’s humanitarian emergency and do not end up being lost to corruption or strengthening the repressive apparatus of the Venezuelan state.

WHO AND WHAT DOES GENERAL LICENSE 41 RESTRICT?

The US Office of Foreign Assets Control (OFAC) regularly issues licenses permitting certain activities that would be restricted by its prior sanctions decisions. The decision to sanction – or, in the precise legal language, to block – certain entities usually emanates either directly or indirectly from executive orders issued by the US presidency. In the case of Venezuela, seven executive orders were issued between 2015 and 2019 and 240 persons and entities were included in OFAC’s list of Specially Designated Nationals (SDN). Importantly, on January 28, 2019, OFAC announced that it would add PDVSA, which holds a constitutional monopoly on the extraction and sales of Venezuelan oil, to the SDN list, therefore barring any transaction between US entities and the Venezuelan oil sector.

The executive orders that serve as basis for these designations are based on the authority granted to the US president through the International Emergency Economic Powers Act of 1977. This law, which has its origins in World War I era legislation to prohibit US entities from trading with the US’s military adversaries, authorizes the president to “block and prohibit all transactions in property and interests in property” of designated entities “if such property or interests in property are in the United States, come within the United States, or are or come within the possession or control of a United States person.”

Claims that Maduro will not receive revenues from the oil sales allowed by the Chevron license are either factually incorrect or highly misleading.

The fundamental idea behind the president’s authority to sanction is that while the US has no jurisdiction to impede non-US actors from doing anything outside of its territory, it can still bar its nationals from being involved in transactions with entities that it believes are acting in a way that is contrary to US national security interests. Note that in order for the executive branch to invoke these powers, it must first argue that the actions of these actors imply an “unusual and extraordinary threat” to US national, foreign policy or economic security and declare a national emergency to deal with that threat. President Obama issued that declaration in March 2015, and all subsequent administrations have extended it by yearly intervals.

In other words, the power of the Treasury Department to sanction non-US entities emanates from the power of the presidency to restrict the economic transactions of US persons – be they firms or individuals – when there are sufficient foreign policy reasons to do so. In the past, US administrations have adopted a relatively lax criteria to define what constitutes a national emergency for the purposes of invoking this authority, allowing it to impose sanctions on a vast array of foreign entities. The US Treasury Department currently lists 38 active sanctions programs, most of which are focused on specific countries or international conflicts.

When an entity is included in the SDN list, all US persons are prohibited from engaging in transactions with that entity. That means, for example, that all bank accounts of that entity in a US financial institution are immediately frozen – as no bank can process a transaction for an SDN unless it receives an OFAC license allowing it to do so. Note that this is not a judicial process in which the SDN is accused of violating the law (although the presumption that it did so may have led to the imposition of the sanctions). Therefore, the assets in question continue to belong to the sanctioned entity. However, the sanctioned entity cannot use these assets in any meaningful way while the sanctions are in place.

The US’s designation of PDVSA in 2019 thus implied that US entities like Chevron were prohibited from doing business with PDVSA or its controlled entities. Because of a provision known as OFAC’s 50% rule, that also means that it could not do business with any entity in which PDVSA has a stake of 50% or more. That includes the joint ventures with PDVSA in which Chevron is a minority partner, Petropiar, Petroboscan and Petroindependencia (which we call the Chevron JVs henceforth).

In the absence of a license, Chevron wouldn’t be able to carry out any financial transactions related to these JVs. Furthermore, the Chevron JVs cannot use the US financial system in order to carry out any transactions. But this doesn’t mean that the Chevron JVs can’t produce oil. On the contrary, the Chevron JVs have continued pumping around 100 thousand barrels per day of oil despite being sanctioned. This is because the US has no legal or real authority to stop a Venezuelan-owned firm from producing oil in Venezuela and selling it outside of the US. Since non-US trade falls outside of its jurisdiction, the most that the US government can do is prohibit firms owned by its nationals from actively participating in that trade. Yet since Chevron is a minority partner in its JVs and has no power to stop the firm’s decision to produce or sell oil, it cannot be accused of having done anything to make these sales possible and cannot thus be found in violation of sanctions because of these sales. And, just in case there are any doubts, prior licenses allowed Chevron to carry out transactions necessary for the “limited maintenance of essential operations, contracts or other agreements” to preserve its Venezuela assets, implying that it was under no obligation to divest from its shares in its JVs nor from its right to receive its share of earnings from these sales.

For exactly the same reasons, the provision of General License 41 prohibiting “payment of any taxes and royalties to the Government of Venezuela” is completely toothless. Chevron does no pay income taxes or royalties to the Venezuelan government because Chevron produces no oil in Venezuela. It is the JVs in which Chevron is a minority partner that produce the oil and pay taxes and royalties to the government of Venezuela and dividends to PDVSA. Chevron has no power to stop the payments made by the JVs in which it is the minority partner because these decisions are taken by the board of the JVs appointed by the majority shareholder, PDVSA – just the same as Chevron has no power to stop these JVs from producing oil in Venezuela. And the US has neither the authority nor the power to stop the boards of the JVs from making the tax and royalty payments that they are obligated to make according to Venezuelan law.

WHO GETS THE MONEY?

According to Venezuelan law, every barrel of oil produced in Venezuela is subject to a royalty payment of 20-33% and an income tax on earnings of 50%. These payments are owed by the firms carrying out the production, i.e., the JVs like Petropiar. Therefore, to answer the question of whether General License 41 leads to an increase in the revenues received by the Maduro government, what we have to answer is whether it will lead to an increase in the production levels or profits of JVs such as Petropiar. (From now on, we will use Petropiar as an example through which we illustrate the mechanisms at work for all the JVs).

The obvious answer is yes. The reason is simple: if taking advantage of the authorizations in the license did not lead to greater profits for Petropiar, then there would be no reason for the Maduro administration to do so. Maduro always has the power to order the JV not to sell oil in the US even if the license allows it. So if Maduro orders the Petropiar board to sell oil to Chevron so Chevron can resell it in the US, then it must be because this generates increased production levels and profits for Petropiar. (This is what we economists call a revealed preference argument: if you see someone doing something, it usually means that that person believes that doing it is to their advantage.)

The US has neither the authority nor the power to stop the boards of JVs from paying the taxes that they are obligated to pay by Venezuelan law.

Furthermore, there is more than abundant evidence that US sanctions have had an effect on Venezuelan oil production, implying that reverting these sanctions, even if only partially, should lead Venezuelan oil production to experience some recovery. In fact, that is the only reason why this decision makes sense from the standpoint of the Biden administration. Accessing US oil markets allows Venezuela to increase oil production because part of the decline of its production was caused by lack of clients willing to purchase Venezuelan oil due to the threat of so-called secondary sanctions (the US ability to sanction third-country firms purchasing Venezuelan oil), and because Venezuela’s inability to obtain key inputs including diluents has been a significant drag on its productive capacity, and the Chevron license explicitly authorizes the firm to import these diluents into Venezuela for the operation of its JVs.

However, the Chevron license also grants Chevron the exclusive right to sell Venezuelan oil in the United States. So, if all the revenue stream from Chevron is precluded from ending up as royalties or taxes to the Venezuelan state, and the additional revenue that the JVs are earning is only coming from sales to the US, how is it that Venezuela can convert these payments into additional fiscal revenues?

To understand the response to this question, it is useful to work through a simple numerical example. First, let’s recall a set of important points. One is that Chevron will never owe royalties or taxes to Venezuela; Petropiar will. The second is that, as is the case for any shareholder, Chevron’s economic benefits from participating in Petropiar are its share of the profits earned by the company. Therefore, any earnings that Chevron receives from the deal are the result of Petropiar earning higher revenues after its tax and royalty payments, as well as other costs, are incurred.

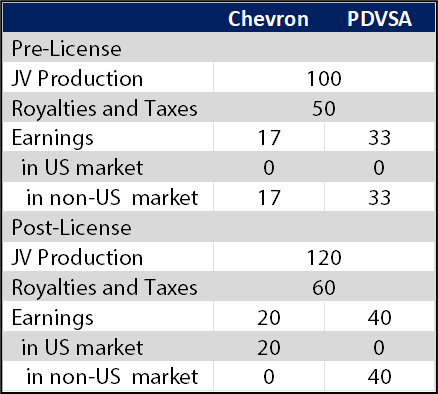

To make the math simple, we will assume that the Venezuelan state takes 50% of all sales proceeds as royalties and taxes, and that before the issuance of the license, Petropiar is producing 100 barrels per day. We also assume away in our calculations any production costs (alternatively, you can think of these numbers as the value of production net of a constant per-barrel cost of production). Then the JV will have earnings after taxes and royalties equal to the value of 50 barrels per day, of which one-third (17 barrels) will correspond to Chevron and the remaining two-thirds (33 barrels) belong to PDVSA.[2]

Because these calculations reflect the distribution of earnings before the issuance of the license, then all of these revenues are generated from sales in non-US markets such as China. These numbers are shown in the upper panel of Table 1.

Now, consider how this changes with General License 41. Let us assume that Petropiar’s production goes up to 120 barrels per day as a result of the opening of these new markets, i.e., that the firm can place through Chevron an additional 20 barrels in US markets. The JV will now pay half of that to the Venezuelan state, and the other half will be distributed among Chevron and PDVSA proportionate to their shares of the company. This means that Chevron will receive 20 barrels per day in earnings, and PDVSA the equivalent of 40 barrels per day, with the remaining 60 going to pay royalties and dividends. But note that Chevron’s 20 barrels are equivalent to the increase in Petropiar’s sales from its ability to sell in the US market.

Remember that Chevron is the only one that can sell oil in the US. So what will happen in practice is that Petropiar will give Chevron these 20 barrels and Chevron will sell them in the US keeping the whole proceeds of the sale. The value of these 20 barrels is exactly what Petropiar has to give Chevron to pay for its profit in the whole firm. Chevron will sell this oil in the US, retain the proceeds in its accounts, and claim that it is in full compliance with US sanctions. American politicians will claim that not one dollar of Chevron’s sales in the US are going to fund the Maduro regime.

Yet consider what has happened to the government take. On the one hand, tax and royalty payments rose by 10 barrels (from 50 to 60); on the other, PDVSA’s earnings after tax and royalties rose by 7 (from 33 to 40). In total, the Venezuelan state increased its revenues by 17, which represents the total Venezuelan take (50% of all production plus two-thirds of profits) of the 20 barrel increase in oil production. While US officials claim that Venezuela is not getting a dime, the reality is that Maduro is keeping 83 cents of every additional dollar generated as a result of opening up US oil markets to Venezuelan oil.

TABLE 1: DISTRIBUTION OF PROCEEDS FROM JV SALES AND EARNINGS, BASE CASE

This simple example illustrates how, because of the fungibility of money, it doesn’t really matter where the revenues of sales in the US “go.” It is, in fact, not difficult for PDVSA to avoid touching the revenues generated by US sales and still make more money from the arrangement. This is because PDVSA can allow Chevron to keep the whole proceeds from its US sales while at the same time keeping a greater share of the proceeds from Petropiar’s non-US sales. And because Chevron as a shareholder has a right only over a given share of the firm’s earnings, then it has no option but to accept that if it is not going to hand over to PDVSA the proceeds from its US sales, it must allow PDVSA to keep the bulk of the proceeds of the non-US sales.

Stopping Chevron from transferring proceeds of US sales to Venezuela does not stop Maduro from receiving more revenues as a result of the agreement.

How does this change if the proceeds of the US sales are applied only to the payment of debt that PDVSA has accumulated with Chevron, as some news media have reported? Note that General License 41 does not mention debt payments at any moment, yet it is believed to be the case that a provision specifying that the proceeds of US sales be applied solely to debt payments could have been included in the contract that Chevron is known to have negotiated with the Maduro government and which has not been made public.

The answer, illustrated in Table 2, is that it doesn’t change much. Note that in our previous example the 20 barrels sold by Chevron in the US market were just enough to cover its share of earnings. If Chevron were to try to use the proceeds to reduce the amount that PDVSA owes it, then it would have to sell more oil in US markets. So let’s now assume that instead of rising by 20 percent, Petropiar production as a result of the deal doubles to 200 barrels. Since Chevron is the only one who can sell in US markets, this means that it must be selling all of the additional 100 barrels in the US. But this would far exceed Chevron’s revenue share in the new situation, which is only 33 barrels. To comply with the agreement and General License 41, Chevron now uses the proceeds from the remaining 67 barrels, which belong to PDVSA, to reduce PDVSA’s debt with Chevron. Thus, Chevron keeps the proceeds from the 100 barrels sold in the US in its accounts and PDVSA reduces its liabilities with Chevron by the market value of 67 barrels.

TABLE 2: DISTRIBUTION OF PROCEEDS FROM JV SALES AND EARNINGS, DEBT REPAYMENT CASE

At one level, the outcome is exactly the same: the Venezuelan state is still getting 83% of all sales, except that it is applying a large part of those proceeds to reduce its liabilities rather than increase its assets. But if we focus just on the cash flow derived from the operation – assuming that reducing liabilities does not benefit Maduro in any meaningful sense – it is still the case that the fiscal take including PDVSA earnings has risen from 83 to 167 barrels, and that even though he has accepted using 67 of those barrels to reduce PDVSA’s debt, Maduro still has seen his positive cash flow increase from 83 to 100. The reason, once again, is that if Maduro accepts that all the proceeds from US sales be used to reduce his debt to Chevron, he acquires the right to use all of the proceeds from non-US sales to pay higher royalties and taxes.

The bottom line is that stopping Chevron from transferring their proceeds of US sales to Venezuela does not stop the Venezuelan government from receiving more revenues as a result of the agreement. This is because what is important to determine Venezuela’s fiscal take is not how much Chevron sells in the United States but how much Petropiar sells as a whole. There is no way to open up markets to Venezuela’s government-controlled oil firms without allowing them to generate additional revenues, revenues in which Maduro can ensure a greater participation even if he commits not to touching one penny of the flows generated in the United States.

However, the fact that the scheme allows Maduro to reap fiscal benefits does not necessarily imply that it gives him all that he wants. Borrowing from the example in Table 2, we could speculate that the government may see an increase in its cash flow of only the value of 17 barrels, when the nation is exporting 100 barrels more to the United States, as too little. In fact, according to some press reports, the government and Chevron had negotiated an agreement in which only one third of the barrels sold by Chevron on behalf of PDVSA would be used to repay debt, a third would be reinvested in the firm and a third would be paid to PDVSA to recoup operational costs.

The problem with implementation of the agreement at present has nothing to do with tax payments – which, as we explained, are not subject to US jurisdiction – but with the ability of Chevron to make the required financial transfers to PDVSA to recoup operational expenses. Recall that General License 41 authorize transactions that are “ordinarily incident and necessary” to the activities that are explicitly authorized, such as extraction and sales of oil. The question is whether reimbursing operating costs of PDVSA is ordinarily incident and necessary to the production and sale of Venezuelan oil. It will likely be up to OFAC to clarify whether these payments qualify as a permitted transaction on these grounds. Note that this problem does not arise with repayment of debts owed by PDVSA to Chevron because OFAC considers debt repayment to be a blocked transaction when a financial institution is involved, which is generally not the case in the payment of commercial arrears.

THE DEMISE OF ACCOUNTABILITY

Since oil sanctions on Venezuela were imposed in 2019, several voices have called for the enactment of an oil-for-essentials agreement that would allow Venezuela to regain access to international oil markets on the condition that institutional mechanisms be designed to ensure that the proceeds from these sales be used to purchase goods and inputs needed to address Venezuela’s humanitarian crisis subject to international monitoring under high standards of transparency. At least three well-designed proposals to this effect were published by non-governmental organizations: Oil for Venezuela (which I direct), the Boston Group and the Atlantic Council’s Venezuela Working Group.

Interestingly, the spirit of these proposals appears to have been incorporated in the Social Agreement subscribed by the Maduro government and an opposition coalition to use funds belonging to the Venezuelan state and until now blocked as a result of sanctions or other measures of economic statecraft such as the non-recognition of the Maduro government by states in which those funds are located.

In contrast, the Chevron license contemplates none of those mechanisms of accountability. Rather, as we have shown in this note, it generates additional cash revenues that the Maduro regime will be able to use at will, and that could easily end up siphoned off to corruption or used to fund the state’s repressive apparatus.

Political expediency may have trumped the concerns with the well-being of Venezuelans that until recently had played such an important role in the US’s foreign policy discourse.

Why the US government opted for this course of action is a difficult question to answer. The explanation that US policymakers did not understand or were not aware of the mechanisms described in this note does not seem credible, given the high stakes involved and the technical expertise deployed by all actors in the development of this solution, which has been negotiated over the course of several months. Rather, the explanation may seem to lie in the complex politics behind the agreement.

In their seminal 1989 book on the political economy of trade policy, Stephen Magee, William Brock and Leslie Young developed the theory of “optimal obfuscation”, which postulated that policymakers would design policies intended to transfer rents to special interest groups while camouflaging them by alleging that they intended to address genuine distributional or efficiency problems. Since voters are unlikely to react kindly to being transparently told that a policy was designed to favor special interests, policymakers will try to come up with arguments that, despite being false or misleading, may yet appear plausible to lay persons who lack the expertise or interest necessary to discern the policy’s true effects. It appears clear that US authorities have been interested in tapping additional sources of oil supply to offset the effect of Russia sanctions and help contain fuel prices. It is also evident that the desire not to antagonize key voter groups, including conservative Cuban and Venezuelan diasporas, has deeply influenced the U.S.’s Venezuela policy. Political expediency may thus have trumped the concerns with the well-being of Venezuelans that until recently had played such an important role in the administration’s foreign policy discourse.

NOTES

[1] Josef Korbel School of International Studies, University of Denver. E-mail: Francisco.Rodriguez4@du.edu. I thank Jacques Bentata, Giancarlo Bravo, Luisa García and Camille Rodríguez for excellent research assistance. Although I am the single author of this paper and assume responsibility for any mistakes, I also wish to recognize that this research is the result of a collective undertaking enriched by the contributions, ideas and insights of colleagues, students and staff. To acknowledge and do justice to their contributions, I write this note in the first-person plural voice.

[2] More precisely, 16.67 and 33.33, respectively.

Excellent report, now just follow where and to whom the money goes?

LikeLike