Between 2012 and 2020, Venezuela’s per capita income fell by 73.8%, the largest peacetime economic contraction documented in the Common Era—and it unfolded under a government that had come to power promising to redirect the country’s wealth toward its poor. We trace how Venezuela’s social policy first expanded, during the oil boom, into a universalisticContinue reading “Social Policy in Venezuela’s Bolivarian Revolution: From Universalism to Politicized Targeting”

Tag Archives: Sanctions

On the implausibility of the benign sanctions hypothesis

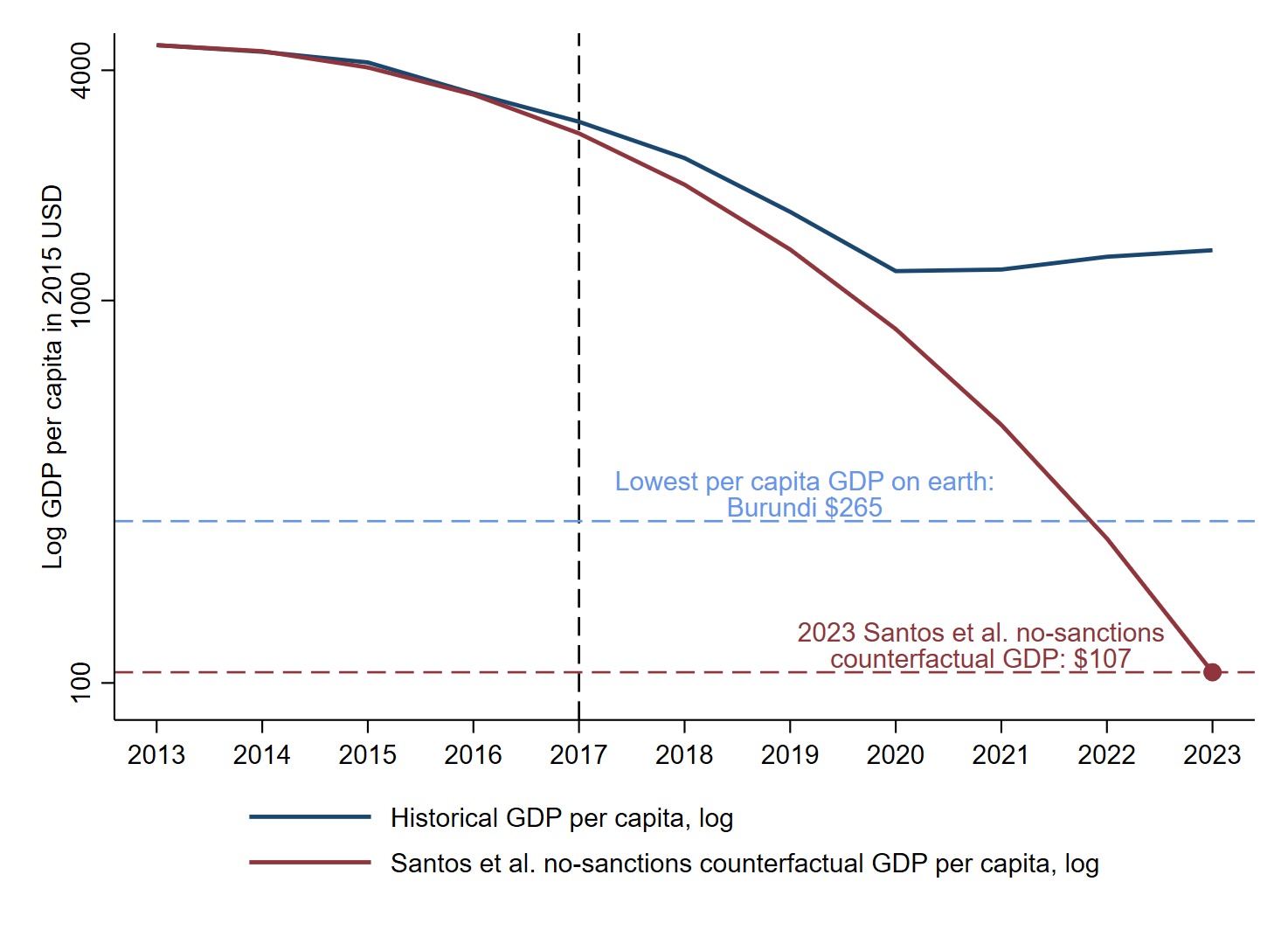

Santos, Morales-Arilla and Partipilo Cornielles (2026) claim that in the absence of sanctions Venezuela’s rate of contraction would have accelerated by approximately 6 percentage points a year. Their projections imply an implausible 98% decline in GDP in a non-sanctions scenario. This would have caused Venezuela’s per capita GDP in the absence of sanctions to fallContinue reading “On the implausibility of the benign sanctions hypothesis”

The Role of Sanctions in Venezuela’s Collapse: A Critical Comment on Santos et al. (2026)

Santos, Morales and Partipilo Cornielles claim that the bulk of the decline in Venezuela’s income preceded the imposition of economic sanctions and that the rate at which the economy contracted did not accelerate after sanctions. Both claims are false. Even if they were true, they would support the authors’ conclusions only if one were toContinue reading “The Role of Sanctions in Venezuela’s Collapse: A Critical Comment on Santos et al. (2026)”

Identifying the effect of the US embargo on the Cuban economy: A comment on Bastos, Geloso, and Bologna Pavlik (2026)

Bastos, Geloso and Bologna Pavlik (2026) argue that the US embargo explains less than one-tenth of the difference in per capita income between Cuba and a counterfactual scenario in which the country did not follow socialist economic policies. We show that their results are driven by the use of an elasticity of income to tradeContinue reading “Identifying the effect of the US embargo on the Cuban economy: A comment on Bastos, Geloso, and Bologna Pavlik (2026)”

Sanctions and Venezuelan Migration

This paper examines the potential impact of different US economic sanctions policies on Venezuelan migration flows. I consider three possible departures from the current status quo in which selected oil companies are permitted to conduct transactions with Venezuela’s state-owned oil sector: a return to maximum pressure, characterized by intensive use of secondary sanctions, a moreContinue reading “Sanctions and Venezuelan Migration”

Scorched Earth Politics and Venezuela’s Collapse

Between 2012 and 2020, Venezuela’s per capita income declined by 71%, the largest peacetime economic contraction documented in the Common Era. I estimate that the severing of the country’s links to global trade and financial markets explains 56% of this contraction. I propose an explanation of Venezuela’s economic collapse as a consequence of the incentivesContinue reading “Scorched Earth Politics and Venezuela’s Collapse”

Sanctions and Human Development

How much have sanctions, and other politically induced restrictions on economic activity, affected the Venezuelan economy? How much of the country’s decline can be attributed to these causes, as opposed to the more standard causes of poor policies and external shocks? In this paper I offer a quantification of the effect of alternative causes. The bottom line is that around half of the country’s economic contraction between 2012 and 2020 can be explained as a result of sanctions and other politically induced restrictions such as the withdrawal of government recognition.

Quantifying Venezuela’s Destructive Conflict

How much have sanctions, and other politically induced restrictions on economic activity, affected the Venezuelan economy? How much of the country’s decline can be attributed to these causes, as opposed to the more standard causes of poor policies and external shocks? In this paper I offer a quantification of the effect of alternative causes. The bottom line is that around half of the country’s economic contraction between 2012 and 2020 can be explained as a result of sanctions and other politically induced restrictions such as the withdrawal of government recognition.

Sanctions and Imports of Essential Goods: A Closer Look at the Equipo Anova (2021) Results

We revisit the results of Equipo Anova (2021), who claim to find evidence of an improvement in Venezuelan imports of food and medicines associated with the adoption of U.S. financial sanctions towards Venezuela in 2017. We show that their results are consequence of data coding errors and questionable methodological choices, including the use an unreasonableContinue reading “Sanctions and Imports of Essential Goods: A Closer Look at the Equipo Anova (2021) Results”

Who Benefits from OFAC’s Chevron License?

In recent days, the US government authorized Chevron Corporation to resell Venezuelan oil in US markets but barred it from making tax and royalty payments to the Venezuelan state. We argue that the restriction on these payments is symbolic because fiscal liabilities are incurred not by Chevron but by the joint ventures in which Chevron is a minority partner and whose decisions it is unable to control. Furthermore, we show that as long as regaining access to US markets enables Chevron joint ventures to increase production levels, the Maduro government will receive additional hard currency revenue flows which it can use at will. This result holds regardless of whether incremental revenues are used to reduce PDVSA’s debt arrears with Chevron.